What are start up costs IRS

Start-up costs include amounts paid or incurred in connection with an existing activity engaged in for profit, and to produce income in anticipation of the activity becoming an active trade or business.

What are examples of start-up costs?

What are examples of startup costs? Examples of startup costs include licensing and permits, insurance, office supplies, payroll, marketing costs, research expenses, and utilities.

What are not start-up costs?

Expenditures that would have otherwise been capitalized, such as the costs associated with the construction of a capital asset, are not startup costs (Rev. … Deductible investigatory expenses include costs incurred for the analysis or survey of potential markets, products, labor supply, and transportation facilities.

What is Section 195 start-up costs?

Common examples of Section 195 start-up expenses include employee training, rent, utilities, and marketing expenses incurred prior to opening a business. … Any start-up expenses that can’t be deducted in the tax year the election is made are amortized over 180 months on a straight-line basis.When can you claim start-up costs?

The business startup deduction can be claimed in the tax year the business became active. However, if you anticipate showing a loss for the first few years, consider amortizing the deductions to offset profits in later years. This would require filing IRS Form 4562 in your first year of business.

Are start-up costs fixed costs?

A realistic start-up budget should only include those things that are necessary to start that business. These essential expenses can then be divided into two separate categories: fixed expenses (or overhead) and variable expenses (those related to producing sales for the business).

Can I deduct start-up costs with no income?

You can either deduct or amortize start-up expenses once your business begins rather than filing business taxes with no income. If you were actively engaged in your trade or business but didn’t receive income, then you should file and claim your expenses.

Can I claim business start-up costs?

Under normal circumstances startup costs are regarded as a capital cost of a business and not tax-deductible. … Because you are conducting your business from home, unless you can find a way that substantiates your claim for electricity and gas related to running the business, you cannot claim these costs.How do I deduct failed start-up costs?

Once you have finished entering your startup costs you will be brought back to the Here’s your [business] info screen. Click the box Add expenses for this work, so to enter other expense categories. You can deduct up to $5,000 of startup costs as a current business expense. The remainder is amortized over 180 months.

Is rent a startup cost?The answer to this question is YES. Believe it or not, rent is actually a start-up cost. … This includes everything from renting office space to paying salaries.

Article first time published onAre LLC startup costs tax deductible?

The Internal Revenue Service (IRS) limits how much you can deduct for LLC startup expenses. If your startup costs total $50,000 or less, you are entitled to deduct up to $5,000 for startup organizational costs.

How do you account for start-up costs?

Debit your startup expense account to increase the total. Credit the asset account you remove the money from. It is important to document your startup costs well. You need accurate records because taxes for startup costs are more complicated than accounting for them.

What is a start-up capital?

Startup capital is what entrepreneurs use to pay for any or all of the required expenses involved in creating a new business. This includes paying for the initial hires, obtaining office space, permits, licenses, inventory, research and market testing, product manufacturing, marketing, or any other operational expense.

What is the difference between startup costs and organizational costs?

Start-up costs include any amounts paid or incurred in connection with creating an active trade or business or investigating the creation or acquisition of an active trade or business. Organizational costs include the costs of creating a corporation or partnership.

How do I deduct startup costs on Schedule C?

How to Claim Start-up Costs. You claim the deduction for start-up costs in Part V of Schedule C (“Other Expenses”). Any excess amount over the first year limit of $5,000 must be amortized over 15 years (180 months). An election to amortize the excess over $5,000 is made by claiming the deduction on Form 4562, Part VI.

Can I deduct start up costs with no income Turbotax?

Turbo Tax will let you enter the expenses without having entered any income. Just continue past, or skip the income part altogether.

How long do you amortize startup costs?

The taxpayer amortizes any startup costs over the deduction limit for 180 months beginning in the month the active conduct of the business to which the costs relate begins (Sec.

What are four common types of startup costs?

Startup costs will include equipment, incorporation fees, insurance, taxes, and payroll. Although startup costs will vary by your business type and industry — an expense for one company may not apply to another.

Are start up costs variable costs?

In contrast to fixed costs, variable costs are start-up costs that are likely to change in line with production or sales volume. If volume increases, variable costs will also increase, but if volumes go down, so will variable costs.

What startup costs can be capitalized?

Start-up costs can be capitalized and amortized if they meet both of the following tests: You could deduct the costs if you paid or incurred them to operate an existing active trade or business (in the same field), and; You pay or incur the costs before the day your active trade or business begins.

What can you claim when starting a business?

- motor vehicle expenses.

- home-based business.

- business travel expenses.

- workers’ salaries, wages and super contributions.

- repairs, maintenance and replacement expenses.

- other operating expenses.

- depreciating assets and other capital expenses.

Is startup money taxable?

Yes, even bootstrapped pre-revenue startups that lose money must pay taxes. You might not be subject to Income Taxes (which are based on profitability) but you will still be subject to a wide variety of other taxes which aren’t always connected to Revenue.

Can you claim formation costs?

“We (being the ATO) consider formation costs (for example, cost of the trust deed to establish an SMSF) are of a capital nature regardless of who pays them. These are not deductible under tax law.

What are pre-opening salaries and wages?

Pre-opening Costs Costs associated with the opening of stores are expensed during the first full month of operations. Preopening Costs Preopening costs, which consist primarily of advertising, occupancy and payroll expenses, are amortized over expected sales to the end of the fiscal year in which the store opens.

What can I write off as an LLC?

- Rental expense. LLCs can deduct the amount paid to rent their offices or retail spaces. …

- Charitable giving. …

- Insurance. …

- Tangible property. …

- Professional expenses. …

- Meals and entertainment. …

- Independent contractors. …

- Cost of goods sold.

What deductions can an LLC claim?

A Corporation or LLC can deduct the cost of travel, lodging, meals, and program fees for employees attending conventions and continuing education. This includes one or more owners employed by the business. The reimbursement is not included in the income of the employee.

Are start-up costs an asset?

In other words, the money you spend for advertising, training employees, legal and accounting expenses and other pre-opening costs are accumulated into one lump-sum “startup costs” and recorded as an asset on your balance sheet.

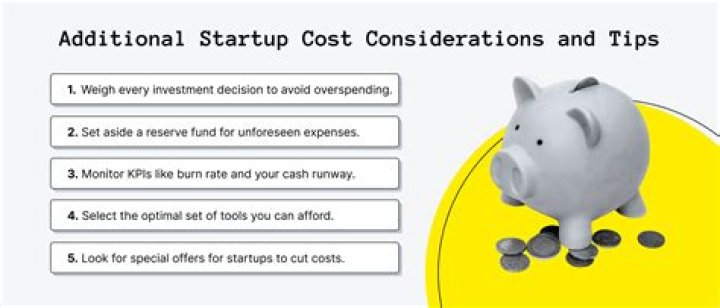

How do you manage startup costs?

- Buy used. …

- Lease instead of buying. …

- Minimize overhead expenses. …

- Hire only who you need. …

- Secure a floating line of credit. …

- Invest in insurance. …

- Form partnerships and barter. …

- Manage your time carefully.

How do bookkeepers do startups?

- Cash basis accounting. …

- Accrual basis accounting. …

- Enter all transactions into your bookkeeping software or Excel spreadsheet. …

- Categorize your transactions. …

- File or digitize receipts. …

- Reconcile your bank accounts. …

- Prepare and send invoices (if applicable) …

- Pay vendors and other bills.

What is the difference between working capital and start up capital?

Working capital is a tool for assessing a company’s cash flow. … Startup capital, on the other hand, is a monetary investment in a corporation for the purposes of product growth, production, expansion, brand management, office space, and inventory.

What are the two types of startup capital?

Types of funding. The two major types of startup capital are equity funding and debt funding although there are a few hybrid flavors as well. Sources of funding. These include venture capital firms, angel investors, crowd-funding, and accelerators/incubators.