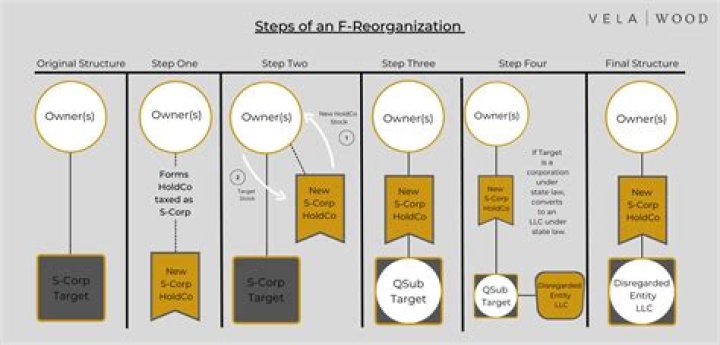

What is an F reorganization

The I.R.C. defines a F Reorganization as “a mere change in identity, form, or place of organization of one corporation, however effected.”[1] This mere change can be accomplished in many ways and for different reasons.

What is the purpose of an F reorganization?

F reorganizations are typically used to effectuate a tax-free shift of a single operating company. They are frequently used as part of a pre-sale strategy or for changing certain undesired attributes of an operating company.

Can a C Corp do an F reorg?

While F reorganizations can also be used with C corporations, an F reorganization is particularly well suited for a variety of transactions involving S corporations. All section references herein, other than to Regulations, are to the Internal Revenue Code of 1986, as amended. Reg. § 1.368-2(m)(1).

Do you need a business purpose for an F reorganization?

As with any Sec. 368(a) reorganization, the F reorganizations in the examples above must have a valid business purpose and satisfy additional judicial doctrines such as economic substance.Do you need a new EIN for F reorg?

The previously assigned EIN should be used by the surviving corporation in a statutory merger and in a reincorporation qualifying as an F reorganization. A new EIN should be requested by the new corporation in a consolidation and in any reincorporation transaction not qualifying as an F reorganization.

Is a name change an F reorganization?

As indicated in Sec. 368, an F reorganization may be effected by changing the identity, form, or place of organization of a corporation. Thus, a change in the name of a corporation could qualify as an F reorganization.

What is a 368 A 1 F reorganization?

Sec. 368(a)(1)(F) provides that an F reorganization is a mere change in identity, form, or place of organization of one corporation, however effected. … The underlying goal is to ensure that only one continuing corporation is involved and that the transaction is not acquisitive or divisive in nature.

What is a tax free reorganization?

Certain types of corporate acquisitions, divisions, and other restructurings which are generally not taxable at the corporate or stockholder level. The transaction must meet strict statutory and non-statutory requirements (see IRC § 368 and Treasury Regulations ).Can an LLC do an F reorganization?

The F Reorganization can facilitate a freeze when you have an existing corporation by creating a two-tier structure where a corporation owns the preferred shares or units of a subsidiary corporation or LLC, and then new common shares or units are issued to new owners/investors in the subsidiary.

What is a QSub election?A parent S corporation uses Form 8869 to elect to treat one or more of its eligible subsidiaries as a qualified subchapter S subsidiary (QSub). The QSub election results in a deemed liquidation of the subsidiary into the parent.

Article first time published onWhat is a Type E Reorganization?

The “E” reorganization is defined as a re-capitalization – the exchanges of stock and securities for new stock and/or securities by the corporation’s shareholders. … In such case, there is a deemed transfer from the old corporation to the new corporation.

Does a QSub file a tax return?

There is no separate federal income tax return for a QSub. Its operations are reported in the S corporation’s federal income tax return, thus providing a de facto consolidated return for the S corporation and its QSub.

Can an S corporation convert to an LLC?

Conversion to an LLC For example, if the S corporation is an entity organized as a corporation under state law, the corporation could file a certificate of conversion with the applicable Secretary of State changing the corporation to an LLC.

What's better LLC or sole proprietorship?

A sole proprietorship is useful for small scale, low-profit and low-risk businesses. A sole proprietorship doesn’t protect your personal assets. An LLC is the best choice for most small business owners because LLCs can protect your personal assets.

Can I get an EIN without an LLC?

You can file for your EIN before forming your LLC, but it is not recommended. If you do not have your LLC registered before applying for an EIN, your application might get rejected by the IRS because it cannot be validated against any state databases.

Do disregarded entities file tax returns?

Does a Disregarded Entity Have to File Tax Returns? Since the owner pays the disregarded entity’s federal taxes on their personal return, the disregarded entity is not required to file a federal income tax return.

What happens to Ein in merger?

A merger occurs when one company with one federal EIN Employer Identification Number is absorbed into a second company with a different federal EIN. For example, in a statutory merger, Corporation M merges into Corporation N.

How do I report a merger on my taxes?

A reporting corporation must file Form 8806 to report an acquisition of control or a substantial change in the capital structure of a domestic corporation. The reporting corporation or any shareholder is required to recognize gain (if any) under section 367(a) and the related regulations as a result of the transaction.

Can an S Corp own a partnership interest?

An S corporation may own an interest in another business entity. … An S corporation can also be a partner in a partnership or a member of an LLC.

Can an S corp own an S corp?

In general, corporations aren’t allowed to be shareholders. The only exception that allows an S corp to own another S corp is when one is a qualified subchapter S subsidiary, also known as a QSSS. … The original business can own the new business as an S corp if it owns all of the shares.

Can two corporations be merged?

You can’t merge a corporation of one state into one from another state. Havaing the VA corporation to be a the sole owner of the two MD corporations is not an option, as an S corp cannot own the stock of another S corp. You don’t need IRS permission, but you will need new federal ID numbers and new S corp elections.

What is a disregarded entity?

A disregarded entity is a business entity that (1) has a single owner, (2) is not organized as a corporation, and (3) has not elected to be taxed as a separate entity for federal tax purposes. The owner of a disregarded entity reports the income of the disregarded entity on the owner’s return.

What is a Type B reorganization?

A type B reorganization as defined in Sec. 368(a)(1)(B) occurs when a parent corporation or its controlled subsidiary acquires the stock of a target corporation solely in exchange for voting stock of the parent corporation.

What is a Type C reorganization?

C-REORGANIZATIONS A C-reorganization, otherwise known as a “practical merger,” is where a target. corporation (“Target”) transfers “substantially all” of its properties to an acquiring. corporation (“Acquiror”) solely in exchange for all or a part of Acquiror’s “voting.

How does a corporate reorganization work?

Reorganization can include a change in the structure or ownership of a company through a merger or consolidation, spinoff acquisition, transfer, recapitalization, a change in name, or a change in management. This part of a reorganization is known as restructuring.

Does a QSub have to file a 2553?

The subsidiary does not file a IRS Form 2553, because a QSSS is not treated as a separate corporation for tax purposes. … Once a valid QSSS election has been made, the subsidiary will not be treated as a separate corporation for federal income tax purposes.

Is an S corporation?

S corporations are corporations that elect to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes. … S corporations are responsible for tax on certain built-in gains and passive income at the entity level.

Can an LLC be a qualified subchapter S subsidiary?

That’s because the income will be taxed at the lower individual taxpayer rate rather than at the corporate rate. An S corporation can create a subsidiary as either a limited liability company (LLC), a C corporation, or a qualified subchapter S subsidiary (QSub).

What is an upstream C reorganization?

An upstream C with a drop is a tax-free upstream Sec. 368(a)(1)(C) reorganization of a subsidiary’s assets (an upstream C), followed by a tax-free contribution of some of the subsidiary’s assets to a new corporation (a drop). The assets not reincorporated are left in the parent corporation’s hands.

What is an acquisitive D reorganization?

Acquisitive reorganizations, as the name implies, involve a restructuring where one corporation acquires another corporation. This can happen via a stock acquisition. With a stock sale, the buyer is assuming ownership of both assets and liabilities – including potential liabilities from past actions of the business.

How do I cancel QSub?

A QSub election can even be revoked before it becomes effective by filing a revocation statement within two months and 15 days of the date the election would have been effective.