What is the temporal method

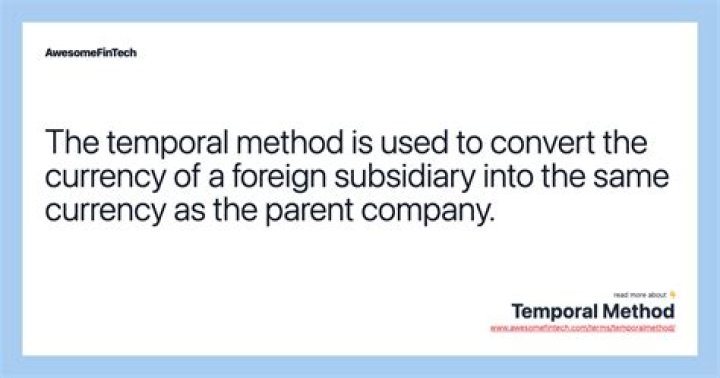

The temporal method (also known as the historical method) converts the currency of a foreign subsidiary into the currency of the parent company. This technique of foreign currency translation is used when the local currency of the subsidiary is not the same as the currency of the parent company.

What is temporal method and current rate method?

Understanding the Current Rate Method The current rate method differs from the temporal (historical) method in that assets and liabilities are translated at current exchange rates as opposed to historical ones. This can create a high amount of translation risk, as the current exchange rate may change.

What is current method?

The “current method” refers to one of 3 approaches (current, temporal, current + temporal) to foreign currency translation. Under the current rate method: Assets and liabilities are translated using the current rate.

What accounts does the temporal method re measure?

The temporal method applies the current exchange rate to all financial assets and liabilities, counting both current as well as long-term. The physical (non monetary) assets which are evaluated at past rates, are translated at past rates.When using the temporal method for translation begin translating the balance sheet and finish with the income statement?

According to the temporal method, the balance sheet must be translated first, followed immediately by the income statement. The temporal method must ensure that there is consistency between the income statement and the retained earnings segment of equity on the balance sheet.

What is the balance sheet exposure under the temporal method?

The balance sheet exposure associated with the temporal method is equal to the foreign subsidiary’s net monetary asset position.

What is the concept underlying the temporal method of translation?

The major concept underlying the temporal method is that the translation process should result in a set of translated U.S. dollar financial statements as if the foreign subsidiary’s transactions had actually been carried out using U.S. dollars.

What is the meaning of functional currency?

A functional currency is the main currency that a company conducts its business. As companies transact in many currencies but report their financial statements in one currency, the foreign currencies have to be translated into the functional currency.What is a subsidiary's functional currency?

What is a subsidiary’s functional currency? The currency in which the entity primarily generates and expends cash. … This is true for the translation process using the current rate method: A translation adjustment is created by the change in the relative value of a sub’s net assets caused by exchange rate fluctuations.

What is meant by the translation of foreign currency financial statements?What is meant by the “translation” of foreign currency financial statements? … It is realized any time the historical exchange rate is different from the spot rate at the balance sheet date.

Article first time published onWhat is meant by closing rate of exchange?

7.2 Closing rate is the exchange rate at the balance sheet date. 7.3 Exchange difference is the difference resulting from reporting the same number of units of a foreign currency in the reporting currency at different exchange rates.

What is current non current method?

In accounting, a convention where all current assets and liabilities in a foreign currency are translated to the domestic currency at the current exchange rate while all long-term assets and liabilities are translated at the exchange rate in effect when each asset or liability was acquired.

What are the two methods used to translate financial statements?

There are two main methods of currency translation accounting: the current method, for when the subsidiary and parent use the same functional currency; and the temporal method for when they do not.

Which method of translating a foreign subsidiary's financial statements is correct?

Which method of remeasuring a foreign subsidiary’s financial statements is correct? Temporal method.

When translating into the functional currency monetary liabilities are translated using the?

For example, monetary items are translated into the functional currency using the closing rate, and non-monetary items that are measured on a historical cost basis are translated using the exchange rate at the date of the transaction that resulted in their recognition. 35.

Which translation method does US GAAP require for operations in highly inflationary countries?

The US GAAP requires a temporal method for operations in highly inflationary countries for translation purposes.

How do you convert financial statements to other currency?

- Determine the functional currency of the foreign entity.

- Remeasure the financial statements of the foreign entity into the reporting currency of the parent company.

- Record gains and losses on the translation of currencies.

What is a company's functional currency quizlet?

What is a company’s functional currency? the currency of the primary economic environment in which it operates.

What is balance sheet exposure?

Definition. A balance sheet exposure is what’s called a “transaction exposure” under U.S. GAAP. They are expected to result in an exchange of one currency type for another and produce un-welcomed foreign currency gains and losses on company financials.

What is translation exposure?

Translation exposure (also known as translation risk) is the risk that a company’s equities, assets, liabilities, or income will change in value as a result of exchange rate changes. This occurs when a firm denominates a portion of its equities, assets, liabilities, or income in a foreign currency.

Why is temporal method used?

The temporal method is used to convert the currency of a foreign subsidiary into the same currency as the parent company. … The currency translation technique allows the parent company to report profits or losses and file financial statements when it has subsidiaries outside of the country where it is domiciled.

What is the difference between remeasurement and translation?

The key difference between translation and remeasurement is that translation is used to express financial results of a business unit in the parent company’s functional currency whereas remeasurement is a process to measure financial results that are denominated or stated in another currency into the functional currency …

How many accounting standards are effective at present?

Accounting Standards (AS 1~ AS 32) have been issued by the Accounting Standards Board of ICAI, to establish uniform standards for preparation of financial statements, in accordance with the Indian GAAP (Generally Accepted Accounting Practices), for better understanding of the users.

Can a company have more than one functional currency?

If those operations are conducted in different economic environments, they might have different functional currencies. Therefore, it is possible for a legal entity to have more than one functional currency, assuming it has several distinct and separable operations, each with different functional currencies.

Which currency is presenting financial statements?

Explanation: International Accounting Standard 21 (IAS 21) defines functional currency as “the currency of the primary economic environment in which the entity operates”. The same Standard defines presentation currency as “the currency in which the financial statements are presented”.

What is the difference between functional and presentation currency?

Functional Currency is the currency of the primary economic environment in which the entity operates. Presentation Currency is the currency in which the financial statements are presented. … Any other currencies in which the entity deals with are foreign currencies.

What is the difference between foreign currency transaction and translation?

Transaction exposure impacts a forex transaction’s cash flow whereas translation exposure has an impact on the valuation of assets, liabilities, etc shown in the balance sheet. … Resulting in different positions on cash flows and balance sheets.

Which translation method do we use when the subsidiary is in a country with highly inflationary economy?

The temporal method is used when a foreign subsidiary operates in a highly inflationary economy. Define remeasurement. Remeasurement is the process of translating the accounts of a foreign entity into its functional currency when they are stated in another currency.

How is cumulative translation adjustment calculated?

Translation Adjustments: To keep the accounting equation (A = L + OE) in balance, the increase of $4,500 on the asset (A) side of the consolidated balance sheet when the current exchange rate is used must be offset by an equal $4,500 increase in owners’ equity (OE) on the other side of the balance sheet.

What is the reporting currency?

Reporting currency is the currency in which an entity’s financial statements or other financial documents are reported. … Most often the currency used is the currency of the country in which the parent company is legally registered.

What is the ratio for exchange of two currencies?

A conversion rate is the ratio between two currencies, most commonly used in foreign exchange markets, which designates how much of one currency is needed to exchange for the equivalent value of another currency. Conversion rates fluctuate regularly for all currencies traded in forex markets.