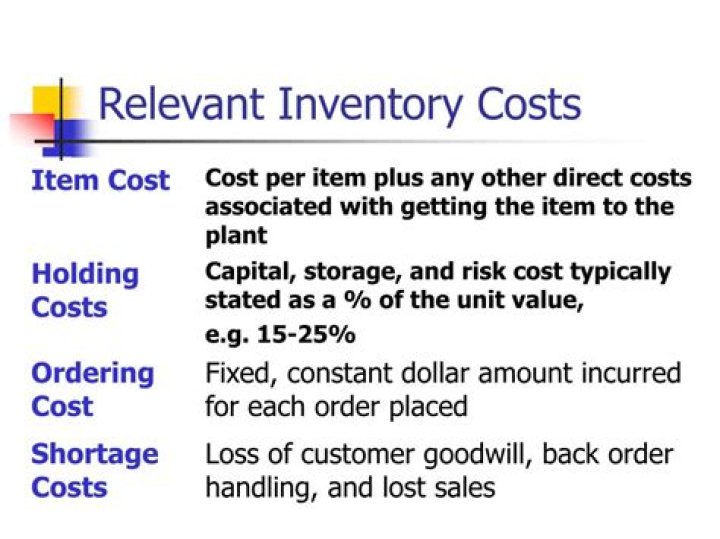

What are the relevant inventory costs

Decisions about how much inventory to hold affect item costs, holding costs, ordering costs, and stockout (shortage) costs. …

What are the 4 inventory costs?

Ordering, holding, carrying, shortage and spoilage costs make up some of the main categories of inventory-related costs.

What are two types of costs associated with inventory?

There are two types of costs associated with inventory: creation/acquisition costs and carrying costs.

What are examples of inventory costs?

These costs include everything necessary to get items into inventory and ready for sale. For example, this can include raw materials, labor, manufacturing overhead, freight-in, certain administrative costs and storage. Accountants usually record inventoriable costs as assets on the balance sheet.What are the types of inventory?

There are four main types of inventory: raw materials/components, WIP, finished goods and MRO.

What are the 5 types of inventory?

5 Basic types of inventories are raw materials, work-in-progress, finished goods, packing material, and MRO supplies. Inventories are also classified as merchandise and manufacturing inventory.

How do you determine inventory cost?

Calculate the cost of inventory with the formula: The Cost of Inventory = Beginning Inventory + Inventory Purchases – Ending Inventory.

What are 3 types of inventory?

Raw materials, semi-finished goods, and finished goods are the three main categories of inventory that are accounted for in a company’s financial accounts.What are the 6 types of inventory?

Inventory exists in various categories as a result of its position in the production process (raw material, work-in-process, and finished goods) and according to the function it serves within the system (transit inventory, buffer inventory, anticipation inventory, decoupling inventory, cycle inventory, and MRO goods …

What are costs of goods?Cost of goods sold is the total amount your business paid as a cost directly related to the sale of products. Depending on your business, that may include products purchased for resale, raw materials, packaging, and direct labor related to producing or selling the good.

Article first time published onWhat is the best inventory costing method?

FIFO in restaurants Of all inventory valuation methods, first-in, first-out is the most reliable indicator of inventory value for restaurants. Because this method corresponds inventory with its original cost, the calculated value of remaining goods is most accurate.

What is inventory cost accounting?

Key Takeaways. Inventory is the raw materials used to produce goods as well as the goods that are available for sale. It is classified as a current asset on a company’s balance sheet. The three types of inventory include raw materials, work-in-progress, and finished goods.

What are the four functions of inventory?

Inventories exist to: (1) to provide and maintain good customer service; (2) To smooth the flow of good through the productive process; (3) To provide protection against the uncertainties of supply and demand; and (4) To obtain a reasonable utilization of people and equipment.

What are the 4 ways of achieving proper inventory control?

- Just-In-Time. One of the most popular methods for inventory management is known as Just-in-Time (JIT) inventory control. …

- Downloading Inventory Software. …

- Stock Control. …

- Reduce Carrying Costs.

What are the 4 questions of inventory management?

- How do I manage a warehouse?

- How do I track inventory in multiple locations?

- How do I get the best value for my money with inventory control software?

- What is the best way to manage inventory?

- What results can I expect from using inventory management software?

How many types of inventory methods are there?

There are three methods for inventory valuation: FIFO (First In, First Out), LIFO (Last In, First Out), and WAC (Weighted Average Cost). In FIFO, you assume that the first items purchased are the first to leave the warehouse.

What is ABC classification of inventory?

ABC analysis is a method in which inventory is divided into three categories, i.e. A, B, and C in descending value. The items in the A category have the highest value, B category items are of lower value than A, and C category items have the lowest value. Inventory control and management are critical for a business.

Which of the following are inventory holding costs?

Holding costs are costs associated with storing unsold inventory. A firm’s holding costs include storage space, labor, and insurance, as well as the price of damaged or spoiled goods. Minimizing inventory costs is an important supply-chain management strategy.

What are the 3 main components of inventory?

Stages of Inventory: Raw materials – materials and components scheduled for use in making a product. Work in process, WIP – materials and components that have began their transformation to finished goods. Finished goods – goods ready for sale to customers.

What are the types of cost systems?

- Type # 2. Absorption Costing:

- Type # 3. Direct Costing:

- Type # 4. Marginal Costing:

- Type # 5. Standard Costing:

- Type # 6. Uniform Costing:

What 5 items are included in cost of goods sold?

- Raw materials.

- Items purchased for resale.

- Freight-in costs.

- Purchase returns and allowances.

- Trade or cash discounts.

- Factory labor.

- Parts used in production.

- Storage costs.

How does inventory affect cost of goods sold?

Understated inventory increases the cost of goods sold. Recording lower inventory in the accounting records reduces the closing stock, effectively increasing the COGS. When an adjustment entry is made to add the omitted stock, this increases the amount of closing stock and reduces the COGS.

What is the difference between cost of goods sold and inventory?

Inventory is recorded and reported on a company’s balance sheet at its cost. When an inventory item is sold, the item’s cost is removed from inventory and the cost is reported on the company’s income statement as the cost of goods sold. Cost of goods sold is likely the largest expense reported on the income statement.

What is the main purpose of inventory?

What Is the Main Purpose of Inventory Management? The primary purpose of inventory management is to ensure there is enough goods or materials to meet demand without creating overstock, or excess inventory.

What are the types of inventory management?

Types of inventory management Typically, inventory types can be grouped into four categories: (1) raw materials, (2) works-in-process, (3) maintenance, repair, and operations (MRO) goods , and (4) finished goods. Try our Inventory management software for your business.

In what ways can Inventories serve to reduce costs to increase costs?

- Get the right reorder point. …

- Make minimum order quantities work for you. …

- Avoid overstocking. …

- Get rid of your deadstock. …

- Decrease supplier lead time. …

- Use inventory management software.

What are the 3 major inventory management techniques?

In this article we’ll dive into the three most common inventory management strategies that most manufacturers operate by: the pull strategy, the push strategy, and the just in time (JIT) strategy.

What are inventory techniques?

Inventory management is a compilation of techniques, strategies and tools for storing, delivering, ordering and tracking inventory or stock.

What is the 80/20 rule in inventory?

The 80/20 rule states that 80% of results come from 20% of efforts, customers or another unit of measurement. When applied to inventory, the rule suggests that companies earn roughly 80% of their profits from 20% of their products.